That is the question to ask when one speaks of speculation, especially for commodities like oil. It is claimed that prices are outrageously volatile, which is true … in part. Prices are volatile, but prices for a market as wide and as complex (information wise) are likely to fluctuate in response to delayed reactions. After all, information about demand and supply in the near future is hard and costly to collect. So yes, there will be volatility.

This is where speculators are useful, they specialize in collecting the information about future demand and supply. In doing so, prices will adjust and the market will use prices as the traffic lights they need about how much inventories to carry, how much to produce, how much is wanted etc. This is because the “futures” contract they buy is basically a bet on future prices – which they specialize in trying to predict. Hence, there might be more small scale fluctuations but they will be less violent and shorter. At least, this is how the theory goes.

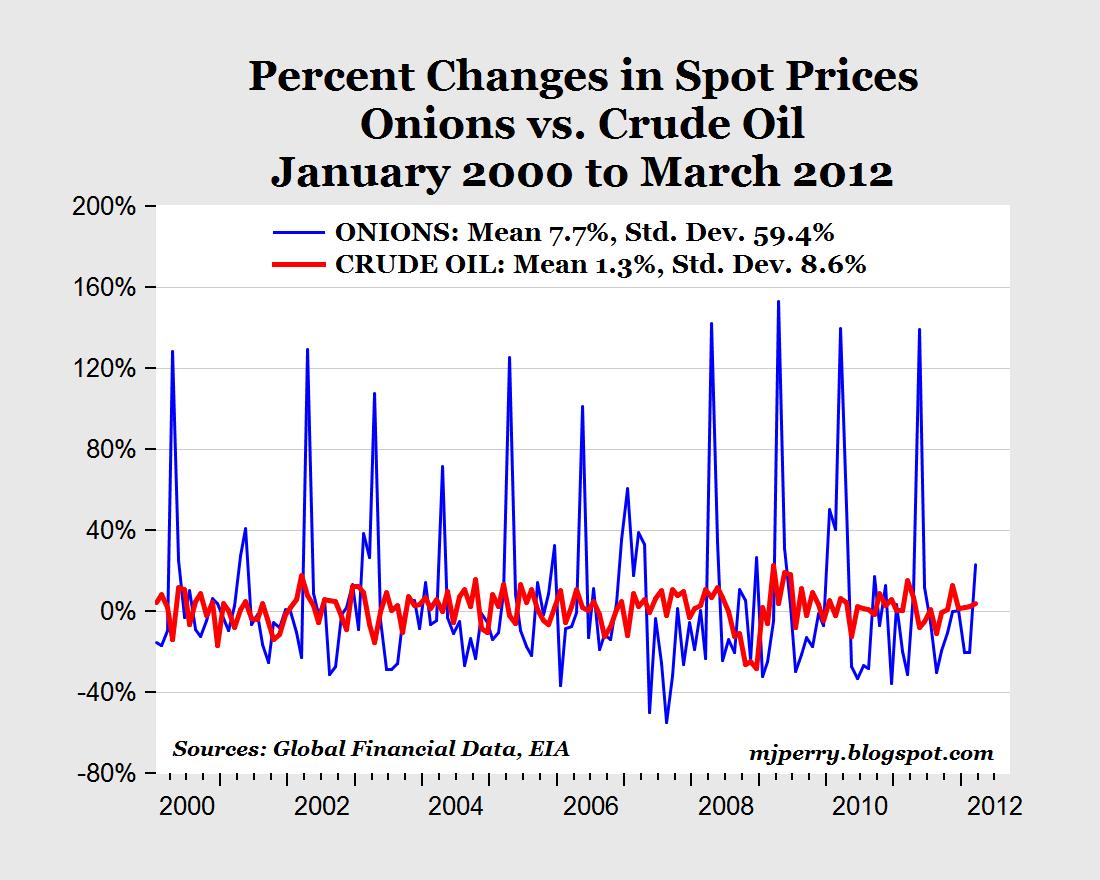

To test this, lets see how violently prices for goods and commodities that are financially traded on futures markets perform relative to those who are not. The two best examples are corn and onions. Onions cannot be traded on futures market since 1958 while corn is trade. As the graph below illustrates (Thanks to MJ Perry), fluctuations are more frequent but considerably less violent for corn than they are for onions. In fact, the same applies for oil and onions (oil prices fluctuate more frequently but less violently).

In fact, when we look at historical examples, we see that there is a very clear case for asserting that speculators cut the amplitude of variations even if they seem to increase the frequency. In a paper in Explorations in Economic History, David Jacks encovers that for the few years in which futures were banned for wheat during the 19th century, prices flucutated more violently than they did with futures.

I understand that it is tempting to blame vile speculators for the current levels of the price of oil, but the blame should rather stand on the shoulders of other factors.

{kind=link}