I have been recently following with deep interest the discussion between Mike Sproul and economist Scott Sumner on whether the backing theory of money is correct or the quantity theory of money (see also David Glasner’s comments). The first being that liabilities on the market (a bond issued by the government) or future income streams are assets against which you can back money. The second being that such assets can hardly be used to issue money. Both sides seem theoretically consistent, but the practical evidence offered by Sproul seems less convincing.

In this debate, Sproul (on a guest blog post at freebanking.org) has come out with an interesting argument with regards to the backing theory using the case of New France (modern day Quebec at the time of French rule, 1608-1760). At the time of New France, the colony was hard-pressed for hard species to pay its troops and the coffers of the colonial administration always ended up being empty mid-year. In 1685, the Intendant opted to issue money on paper notes (on the back of playing cards) that would be backed by future shipments of gold. All notes would eventually be redeemed by the administration. Using this case, Sproul argues the following in support of the backing theory :

Suppose that the government owed 30 livres [a livre being the currency unit] of back pay to each of 1,000 soldiers, for a total of 30,000 livres of wages payable. Suppose also that a shipment of 30,000 livres in coin was due to arrive from France after three months. A prudent strategy for the intendant would be to first issue 10,000 paper livres, pay 10 livres to each of the soldiers, and promise that each paper livre would be redeemable for 1 livre in coin when the coins arrived from France. Assuming this initial issue went well, he could then issue the other 20,000 paper livres and pay each soldier the 20 livres still owing (…)

ASSETS LIABILITIES

1) 30,000 lvs. coins (due from France) 30,000 lvs. wages payable 2) +10,000 lvs. paper paid to soldiers -10,000 lvs. wages payable 3) +20,000 lvs. paper paid to soldiers -20,000 lvs. wages payable 4) +1000 lvs. (government bond) +1000 lvs. paper spent on a bond 5) +2000 lvs. IOU from a farmer +2000 lvs. paper lent to a farmer So far, the colony’s monetary activities can be summarized in lines 1-3 of the T-account above. Line 3 raises an interesting question: The 20,000 livres issued in line 3 tripled the quantity of paper money, from 10,000 to 30,000 livres. Would this cause inflation? The quantity theory of money suggests that it would, since there would be three times as much money chasing the same goods. But there is another theory, the backing theory of money, which says that the 30,000 paper livres are adequately backed by 30,000 in coins due from France, so each paper livre must be worth 1 livre in coin. Furthermore, suppose the colony issued another 1000 paper livres and used them to buy a French government bond worth 1000 livres (line 4), and then issued another 2000 paper livres and lent them to a farmer (line 5). The backing theory still says there would be no inflation, since the 33,000 paper livres would be adequately backed by 33,000 livres of the issuer’s assets. Of course, if that 1000 livre bond turned out to be worthless, and if the farmer defaulted on his loan, then the 33,000 paper livres would be backed by only 30,000 livres of assets, and the backing theory would imply about 10% inflation.

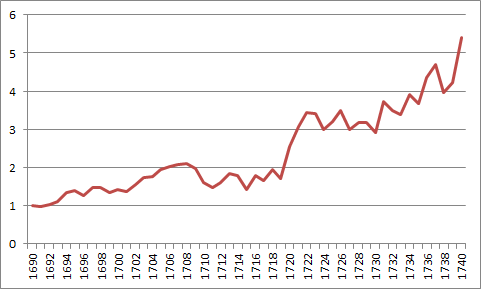

Again, as I mentionned in the introduction of this post, I believe that theoretically the case makes sense. However, having worked on Canadian economic history and currently being in the process of producing a GDP series and a price index series from 1680 to 1860, I can argue whether or not Sproul is correct. Let us focus on the years prior to 1719 – the first experiment with paper money in the colony. Here is my price index (with 1720-1724 =100):

PRICE INDEX FOR NEW FRANCE, 1688 to 1760 (1720-1724=100) / log scale

GDP OF NEW FRANCE, INDEX VALUES = 1690=1

What we have is the following: a massive price increase up to 1719 and slow growth up to 1719 (below population growth). I think that these undermine the backing theory of money considerably. When the colonial administration increased the monetary base by issuing money backed against future shipments of gold and silver and/or stocks in fur companies, it was in effect doing exactly what central banks do today when they buy government bonds. At first RGDP will increase alongside prices, but eventually, all that one will be left with is higher prices and lower output. That is exactly what happened in New France : prices and GDP rose at first and eventually, growth petered off because of excessive money creation.

Here, Sproul could argue that my line of reasoning occurred once note-holders realized that the notes were backed against nothing of real value or of great risks. But this line of reasoning does not hold its ground to historical facts. Discounting on notes emerged even in the first issuance of 1685. Using account books from religious orders, I find that discount rates were always between 10% and 20% of the face value of notes up to 1704 and increased to roughly 40% thereafter. This is because the risks associated with the assets that backed the money determined the quantity of money. If merchants, in time of war, felt that the gold could be seized at sea, they would only accept notes at a higher discount. In this situation, individuals who held notes would simply find no one to trade with for these notes. Hence, the money stock declined because of hoarding (albeit undesired hoarding). If risks declined, the discount rate would decline and more notes would re-enter circulation. Since the exchange rate between species and notes was unregulated between 1685 and 1714, the stock of money varied according to the risks associated with playing cards (which in turn affected the exchange rate between notes and gold).

Moreover, the fluctuations in the risks associated with the assets would also have impacted the velocity of money. Imagine the following situation. At period zero, the farmers of New France held only hard currency. At period one, the government issued notes at zero risk. At the end of period one, individuals had diversified portfolios of notes and currency as cash holdings. At period two, the risk associated with the notes increases and so does the discount rate on these. Individuals are left with cash holdings whose value is not representative of their desires. To return to their cash reserves preferences, they can sell assets – increasing the number of transactions during period three. Hence, velocity has changed. The system was a tributary of monetary disequilibriums in New France.

Although there are some important merits to the “backing theory” of money, the example of New France is not a great supporter of this case.

What is the unit of your price index? Livres?

I can understand, using the QTM, why the price level rose following the issuance of paper notes, but do you have any theory as to why came back down? Did the Intendant simply nullify his promise to redeem them? Surely there would be some historical account of such a decision.

Livres (monnoye du pays).

The 1714-1719 hike was the result of the governor plan of redemption. By setting the redemption rate at half the value, all the notes that were worth less (somewhere between 60% and 70% discount in 1713) were just hoarded in households. Once the governor said, I’ll pay you back by half – all the notes flooded the market and because the new exchange rate was fixed (unlike prior to 1714), you had inflation.

I think the 1703-1709 drop is mostly the result of a massive shock to household balance sheets (Great Depression style deflation). Because the notes could be traded at market exchange rate, the discount rate that they demanded was so high that no one wanted them. All holders of such notes saw their household net worth drop massively. They were stuck with assets denominated in livres that no one wanted. This is exactly like Leland Yeager’s 1953 “A Cash-Balance Interpretation of the Great Depression” in the AER.

Sorry I didn’t see this post earlier, but for what it’s worth, here is my response:

The backing theory is, unfortunately, difficult to test empirically. For example:

“When the colonial administration increased the monetary base by issuing money backed against future shipments of gold and silver and/or stocks in fur companies, it was in effect doing exactly what central banks do today when they buy government bonds. At first RGDP will increase alongside prices, but eventually, all that one will be left with is higher prices and lower output. That is exactly what happened in New France : prices and GDP rose at first and eventually, growth petered off because of excessive money creation.”

The backing theory says that when more money is issued at the same time that more assets are pledged as backing for that money, there will be no change in prices or in RGDP. It also says that if the government issues more money while not getting enough backing in return, then there will be inflation.

In my paper “There’s No Such Thing as Fiat Money”, I discuss the empirical work of Sargent, Smith, Cunningham, Calomiris, etc, all of whom found ways to test the backing theory against the quantity theory. They concluded that the backing theory fits the data better than the quantity theory.

intéressant